America’s debt and deficits are stirring up markets in ways we haven’t really seen in years. Long-term interest rates are popping (think higher mortgage rates), even despite some positive trade deal chatter. Just last week, Moody’s lowered the U.S. credit rating, and yesterday’s weak 20-year Treasury bond auction sent up another red flag.

What’s Driving This?

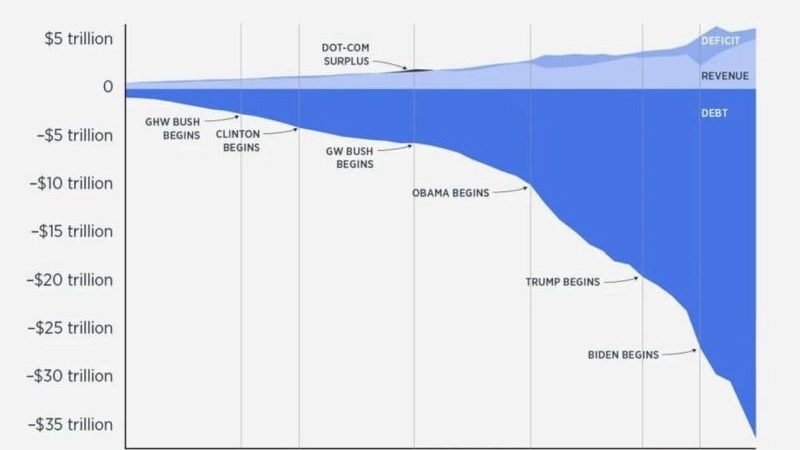

I’ve been talking about the U.S. debt-to-GDP ratio for a while now, as it has been on an unsustainable path. The 2024 budget deficit came in at $1.8 trillion (6.4% of GDP), and the CBO projects we are looking at $2.1 trillion deficits annually for the next decade. Here is the thing: we’re spending like it’s a crisis, but there is no current recession, war, or pandemic. DOGE came in to help cut the deficit, but now there’s talk of adding $4 trillion more to the budget. With U.S. Treasury debt at $36.2 trillion, we’re spending $1.2 trillion a year in interest payments alone, 40% more than the $850 billion defense budget. The CBO warns publicly held debt could hit 150% of GDP by 2055.

What the Markets Are Saying

The bond market has moved front and center. Long-term yields may no longer be strictly within the Fed’s control, signaling doubts about our fiscal path. It’s not just us… Japan’s rates are climbing after years near zero, and gold’s surge has caught many investors by surprise. Recently, there’s been a shift into alternative forms of money, and investors with only a recent memory of market behavior may not fully grasp these shifts. As Ray Dalio famously said, “If you don’t own gold, you know neither history nor economics.”

Where Do We Go From Here?

Talk of tax cuts, rate cuts, and fiscal stimulus is bumping up against a bond market that’s demanding financial discipline. Markets could grow anxious as valuations remain historically high while bond yields pressure relative valuations of competing assets. As I wrote in my recent Kiplinger’s piece, the “old playbook might not cut it”.